Amazon (NASDAQ: AMZN) is poised to release its second-quarter 2025 earnings after the closing bell, with Mag 7 peers Microsoft and Meta both having posted beat and raise quarter’s in the past 24 hours.

The consensus anticipates revenue of $162.11 billion, a 9.55% sales growth rate year-over-year, and earnings per share (EPS) of $1.33, up from $1.26 in the same quarter last year.

X testing X

WELCOME BONUS - Free Share Bundle When You Invest £50!

Get up to £500 cashback for investing with IG.

Invest in 15,000+ shares and ETFs. Open an account now, invest at least £50, and you’ll get a free share bundle worth between £40 and £200. T&Cs apply.

5.0

Open Account

Spread bets and CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading spread bets and CFDs with this provider. You should consider whether you understand how spread bets and CFDs work, and whether you can afford to take the high risk of losing your money.

However, following a Q1 report where Amazon beat top-line estimates but offered conservative operating income guidance due to tariff anxieties and cost pressures, the market’s reaction will hinge on more than just headline numbers.

Prime Day, expanded to a four-day event, is projected to provide a significant boost to retail sales, but some analysts caution that lower average selling prices could potentially moderate the impact on overall profitability.

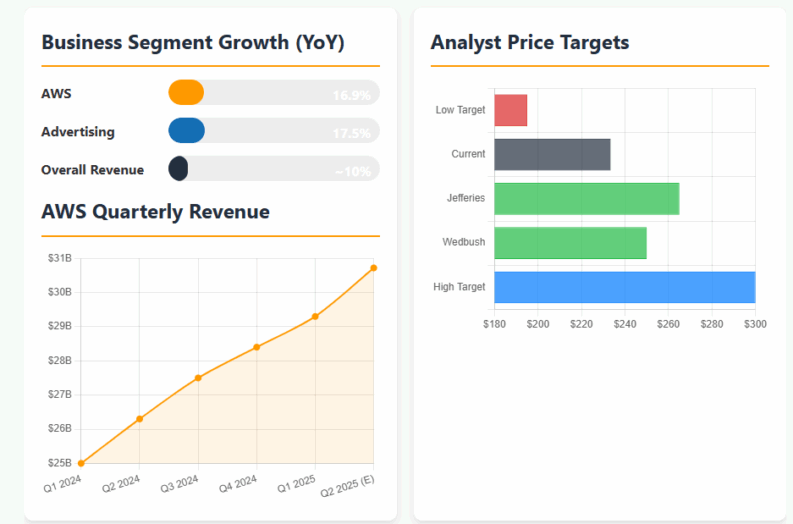

Amazon Web Services (AWS) remains a focal point. In the first quarter, AWS revenue surged 17% year-over-year to $29.3 billion, boasting an impressive operating margin of 39.5%. Projections for Q2 estimate AWS revenue at $30.72 billion, indicating a 16.9% year-over-year growth.

The recent introduction of Amazon Nova models, including the Nova Sonic speech-to-speech foundation model and the Nova Act SDK, has bolstered AWS’s AI capabilities. Furthermore, the deployment of Trainium 2 chips, promising enhanced price performance for AI workloads, is expected to strengthen AWS’s competitive edge.

“We are constructive on the setup ahead of the report given encouraging U.S. retail data, healthy advertiser sentiment, strong AWS demand, and continued efficiency gains across the business that should drive upside to margin expectations,” notes Scott Devitt, Wedbush analyst, who raised the firm’s price target on Amazon to $250 from $235.

However, the shadow of trade policies looms large. With approximately 60% of its revenue derived from North America, Amazon is particularly vulnerable to tariff fluctuations. Management has consistently emphasized the uncertainty created by evolving trade policies, and analysts warn that escalating tariffs present a challenging dilemma: absorbing the costs could squeeze profit margins, while passing them on to consumers may dampen sales.

Amazon’s advertising segment continues to be a bright spot in its financial portfolio.

In the previous quarter, the advertising business generated $13.93 billion in revenue, demonstrating a robust 17.7% year-over-year increase, outpacing even AWS as Amazon’s fastest-growing business. Citi projects that Q2 advertising revenue will expand by 17.5% year-over-year, excluding exchange rate effects.

Jefferies analysts have also expressed optimism, raising their price target for Amazon to $265, citing resilient revenues, cost discipline, and stable consumer demand as key drivers. They maintain a ‘Buy’ rating on the stock, suggesting that despite recent gains, shares still present an attractive upside.

A 5.6% gain for the stock YTD is by no means disastrous, but it does have AMZN lagging markets leading in. Spare a thought for holders of another of the Mag 7 names in Apple, also slated to release earnings tonight, down 14% YTD.

With other tech names having delivered scorching earnings reports fresh in the memory, the pressure is on Amazon to show that it can keep up. Missed beats have been harshly punished by markets, and an inkling of weakness could see AMZN held up whilst others race ahead.

Searching for the Perfect Broker?

Discover our top-recommended brokers for trading or investing in financial markets. Dive in and test their capabilities with complimentary demo accounts today!

The AskTraders Analyst Team features experts in technical and fundamental analysis, as well as traders specializing in stocks, forex, and cryptocurrency.

WELCOME BONUS - Free Share Bundle When You Invest £50!

Get up to £500 cashback for investing with IG.

WELCOME BONUS - Free Share Bundle When You Invest £50!

Get up to £500 cashback for investing with IG.