Daimler Truck Holding AG, a global heavyweight in the commercial vehicle sector, is getting sets to report its Q1 2025 earnings tomorrow (May 14), with sentiment shifting bullish leading into the print. The recent DTG stock (ETR: DTG) performance has been strong, with a 17.45% rally over the past month of trading moving Daimler Truck AG back in sight of €40.

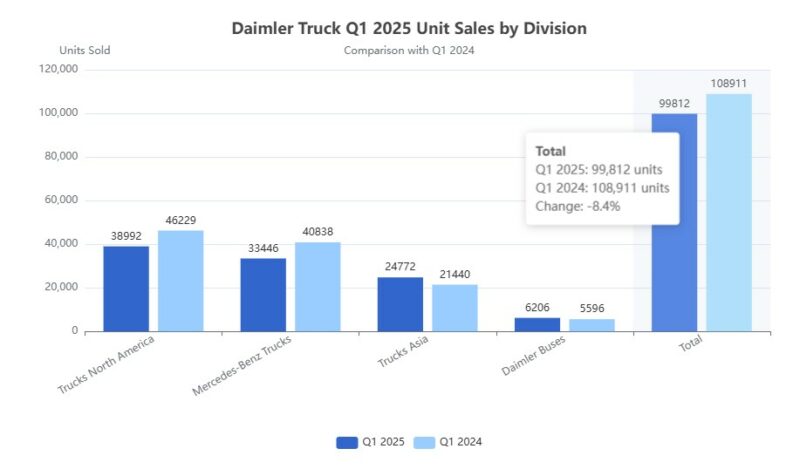

Q1 2025 unit sales highlight the company’s regional divergence. Total units sold fell 8% year-on-year to 99,812, with North America and Europe posting sharp declines (down 16% and 18%, respectively), while Asia and the Daimler Buses segment posted double-digit growth. Battery-electric vehicle sales remain a challenge, down 7% year-on-year, though the company continues to invest heavily in zero-emission platforms, including the GenH2 hydrogen truck and eActros 600.

Strategic partnerships such as those with ARX Robotics and 3D Systems aim to diversify revenue streams and enhance efficiency. Meanwhile, the potential merger of Hino Motors and Mitsubishi Fuso Truck and Bus could unlock synergies in Asia.

WELCOME BONUS - Free Share Bundle When You Invest £50!

Get up to £500 cashback for investing with IG.

WELCOME BONUS - Free Share Bundle When You Invest £50!

Get up to £500 cashback for investing with IG.

Management’s guidance for 2025 anticipates industrial revenue of €52–54 billion and adjusted EBIT growth of 5–15%, contingent on stabilizing demand in Europe and sustained resilience in North America. The upcoming Capital Markets Day on July 8 is expected to clarify restructuring plans for the underperforming European business.

Daimler Truck’s financials paint a picture of a value-oriented industrial giant under pressure. The company trades at a trailing P/E of 9.77 and a forward P/E of 7.91, with price-to-sales and price-to-book ratios of 0.56 and 1.31, respectively. These metrics signal relative undervaluation, particularly given trailing-twelve-month revenues of €54.08 billion.

Yet, the company is not immune to industry challenges. 2024 saw a 3.24% drop in revenue and a sharper 23.18% fall in net income, as European demand faltered and supply chain disruptions persisted. The EBITDA margin contracted from 11.44% in 2023 to 9.98% in 2024, with North America, a region responsible for 37% of group revenue, facing inventory corrections and weaker freight demand.

Despite earnings headwinds, Daimler Truck has reaffirmed its commitment to shareholder returns. The company will pay a €1.90 per share dividend on May 28, yielding 4.56% (forward yield: 5.68%), supported by a payout ratio of 52%. An ongoing €2 billion share buyback program, of which €968 million remains, further underpins investor confidence. Free cash flow rose 12% to €3.15 billion in 2024, providing ample liquidity for these initiatives.

The analyst consensus remains cautiously optimistic. The average price target stands at €44.14, implying over 10% upside from current levels, with a “Moderate Buy” rating. However, concerns linger. Barclays recently downgraded the stock to “Equalweight,” citing delays in cost-saving initiatives and persistent European market weakness.

While near-term headwinds persist, the company’s strategic investments, dividend consistency, and buyback program position it for long-term value creation. We will be looking for any updates on European restructuring and Q1 margin performance in tomorrow’s report.

Searching for the Perfect Broker?

Discover our top-recommended brokers for trading or investing in financial markets. Dive in and test their capabilities with complimentary demo accounts today!

- IG Top-tier regulation – Read our Review

- eToro Wide range of instruments available to trade – Read our Review

YOUR CAPITAL IS AT RISK. 76% OF RETAIL CFD ACCOUNTS LOSE MONEY