The UK supermarket sector in 2025 has been a study in contrasts. Share prices of the nation’s largest listed grocers Tesco (LON: TSCO), and Sainsbury’s (LON: SBRY), have been moving at odds to Marks & Spencer (LON: MKS), and Ocado (LON: OCDO) since the start of the year.

Whilst the YTD gains for Sainsbury’s and Tesco are remarkably similar, over the 1 year time-frame, there is a clear winner, with Tesco’s shares having gained 23.67%, whilst SBRY has added 2.83%.

We take a look at how the market has been developing this year, along with the overarching themes that have been driving the sector in different directions.

WELCOME BONUS - Free Share Bundle When You Invest £50!

Get up to £500 cashback for investing with IG.

WELCOME BONUS - Free Share Bundle When You Invest £50!

Get up to £500 cashback for investing with IG.

| Key Insights | |

|---|---|

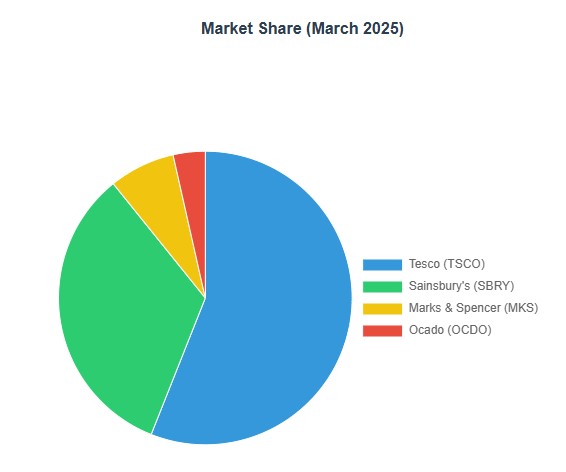

| Market Leaders | Tesco and Sainsbury’s continue to dominate with a combined 43.1% market share |

| Price Performance | Tesco has outperformed the sector, while Ocado has struggled |

| Premium Strategy | M&S has capitalised on premium trends and special occasion spending |

| Cost Pressures | All supermarkets face headwinds from increased National Insurance and higher minimum wages |

| Competition | Discounters like Aldi (11% market share) continue to put pressure on the traditional players |

Tesco (LON: TSCO)

Tesco shares fell sharply in April 2025 reaching a low of £3.14, reflecting investor concerns about profit margins in the face of a price war and rising costs. In spite of reaching such a low, the share price since the beginning of the year has increased 2.66%.

The company reported lower pre-tax profit for FY25 and issued a cautious outlook for FY26, though it did increase its dividend and announced a £1.45 billion share buyback, possibly to bolster shareholder confidence.

Tesco, the UK’s largest supermarket, entered 2025 with a commanding market share near 27%. Its operational performance in the early part of the year was underpinned by resilient grocery sales and a robust pricing strategy that helped it maintain and even grow share at the expense of rivals such as Morrisons and Asda. However, the competitive landscape shifted dramatically in April, when Asda launched a new “Rollback” discounting campaign and Tesco itself warned of intensifying price competition. This triggered a sharp sector-wide sell-off, with Tesco shares dropping over 6% in early April as investors digested the company’s cautious outlook and concerns about squeezed margins.

Operationally, Tesco faces significant cost headwinds. Increases in employer National Insurance contributions and the UK’s higher national living wage have driven up expenses for the sector’s largest employer. Despite these challenges, Tesco has sought to support its share price through a £1.45 billion buyback and a dividend increase, signaling management’s confidence in the company’s long-term prospects. Yet, the near-term outlook remains clouded by the specter of a prolonged price war and margin pressure.

Sainsbury’s (LON: SBRY)

Sainsbury’s, the UK’s second-largest grocer with a market share of around 16%, has demonstrated solid operational momentum in 2025. The company’s “Next Level” strategy, which saw a £1 billion investment in price reductions, delivered its strongest market share gains in over a decade. Like Tesco, Sainsbury’s has matched discounter pricing while maintaining a premium product focus, helping it retain and grow its customer base even as consumer confidence remains fragile.

Sainsbury’s share price has kept up its momentum since the beginning of 2025 by rising 3.05% since January. The April sell-off did not spare Sainsbury’s, whose shares fell 4.4% reaching a low of £2.39 in sympathy with Tesco.

Nevertheless, its operational performance and market share gains suggest a degree of resilience, with analysts highlighting its successful navigation of both cost inflation and competitive threats. Sainsbury’s remains well-positioned to weather ongoing volatility, provided it can continue balancing cost management with value-driven customer offerings.

Marks & Spencer (LON: MKS)

Marks & Spencer had been emerging as a relative winner in 2025, particularly in its food division. The company capitalised on consumer trends toward premium products and “special occasion” spending, reporting robust sales growth over the festive period and into the new year. M&S’s dual focus on food and clothing has helped it rebound from previous years’ volatility, with its stock showing a strong recovery and trading above key moving averages.

However, Marks & Spencer’s share price in the recent weeks and months has slowly declined as the company battles cyber attacks on their retail division in late April that has impacted margins.

Operationally, M&S is not immune to sector-wide cost pressures. Rising employment costs threaten to erode margins, and the company’s premium positioning may face challenges if consumer spending weakens further. For now, though, M&S stands as a testament to the value of targeted operational strategy and brand strength in a difficult market.

Ocado (LON: OCDO)

Ocado’s 2025 story is markedly different. After a brutal 2024, which saw the share price fall nearly 60%, the online grocer has continued to struggle. The share price since the beginning of January 2025 has fallen -15.42% and is still not close to its 52-week high of £4.93.

Its market share has slipped to 1.7%, and the company’s exit from the FTSE 100 underscored persistent investor skepticism about its long-term prospects. While consumer spending via Ocado rose 4% year-on-year, this was not enough to offset concerns about profitability and the viability of its technology licensing model.

Ocado’s share price remains well below long-term averages, and while recent months have seen some stabilisation, analysts remain cautious. The company’s online-only model faces headwinds as consumers return to in-store shopping, and established grocers ramp up their own digital offerings.

Key Sector-Wide Themes

- Market Share Stability: Tesco and Sainsbury’s continue to dominate, though discounters Aldi and Lidl are steadily growing their presence, with Aldi reaching an 11% market share by March 2025.

- Cost Headwinds: All major supermarkets are grappling with increased employment costs due to changes in National Insurance and higher minimum wages, impacting profitability.

- Competitive Intensity: The return of aggressive price competition, especially from Asda and the discounters, has put pressure on margins and weighed on share prices across the sector.

- Online and Technology: Ocado’s struggles highlight the challenges faced by online-only models post-pandemic, especially as consumers return to in-store shopping and competition intensifies from established grocers’ own digital efforts.

2025 has proven to be a year of both opportunity and challenge for UK supermarket stocks. Tesco and Sainsbury’s remain sector leaders, but face mounting pressures from discounters and rising costs. Marks & Spencer’s strategic focus on premium segments has delivered a strong rebound, although recent events have shifted the tide.

With sector-wide sales growth slowing to just 2.7% and competition fiercer than ever, the outlook will depend on each company’s ability to balance value, cost control, and operational agility in a rapidly changing retail environment.

Searching for the Perfect Broker?

Discover our top-recommended brokers for trading or investing in financial markets. Dive in and test their capabilities with complimentary demo accounts today!

- IG Top-tier regulation – Read our Review

- eToro Wide range of instruments available to trade – Read our Review

YOUR CAPITAL IS AT RISK. 76% OF RETAIL CFD ACCOUNTS LOSE MONEY